Although bank branches have been on the decline for years, in the wake of the global pandemic, widespread adoption of mobile and online banking has resulted in an even sharper drop. But these modern banking services have their limits, and bank customers inevitably must visit a branch for any number of advanced transactions. So how do banks balance this need to rationalize branches with customers’ demands for adequate access to financial services?

For South Korea, the answer seems to lie in the collaboration between convenience stores and bank branches. According to the Financial Supervisory Service, South Korean banks have closed an average of 200 branches per year since 2019, whereas the Asian Business Daily reports that nearly 2,000 new convenience stores have been opened yearly during this same time frame. This sharp uptick in convenience stores has made them a prime real estate opportunity for banks looking to maintain their physical presence. The result is numerous retail-bank alliances cropping up all around the country to provide self-service banking operations in more convenient locations outside traditional banking hours. But how do they operate? What are the advantages? A closer look at the biggest banks in Korea can reveal the success of these new branch formats, as well as lessons for potential adoption in other countries.

Shinhan Bank’s Drive for Innovative Convenience

As one of the top banks in South Korea, Shinhan Bank has long been a pioneer of banking technology. That’s why it was no surprise that they were the first ones to implement the convenience store-bank branch hybrid format with their ‘Innovation Stores’. For Shinhan Bank, it’s about providing their customers with the utmost in banking experiences, while keeping operational costs down. To do this, the bank has partnered with local convenience store chain GS25 to open several shared convenience store bank branches throughout the country.

Powered by the latest technologies from Hyosung, these mini-branches are able to provide customers with nearly all the services of a traditional bank branch in a more on-the-go format, while also increasing footfalls for the convenience store business. The Digital Desk™ from Hyosung, operates until 8pm – well after typical branch hours – to connect customers with Shinhan Bank’s digital sales personnel who can help them remotely conduct a number of transactions such as account openings, loan applications, and more. The inclusion of Hyosung’s Digital Kiosk also allows customers to make deposits and handle other more routine bank transactions, all with the comfort of self-service automation. With Hyosung solutions acting as the heart and soul of these Innovation Stores. Shinhan Bank is able to meet their customers where they are, provide them with comprehensive banking experiences, and drive down operational costs resulting in 20.8% more visits during the first 6 months of the store opening (FETV, 2022).

Kookmin Bank Seeks to Extend Banking Services

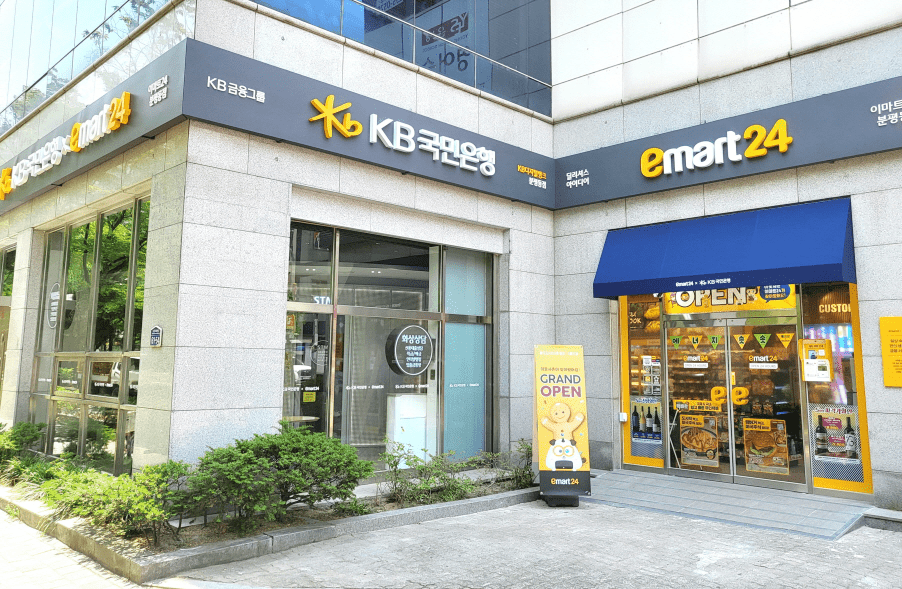

Elsewhere in South Korea, Kookmin Bank has partnered with GS25 rival, Emart 24, to implement similarly innovative retail store branches. In the case of Kookmin Bank, the goal has been to expand their branch services through the implementation of smart teller machines (STMs) and the Digital Desk™ from Hyosung. Through the STMs, customers can visit the nearest Emart 24 convenience store until 7pm to issue passbooks and debit cards, make cash and check deposits, and even manage security cards and OTP devices.

On the other hand, the Digital Desk™, much like for Shinhan Bank, allows Kookmin Bank to extend its consultative service hours and provide customers with comprehensive remote banking consultation. In fact, Kookmin Bank has deployed the Digital Desk™ as the centerpiece at several retail locations such as small supermarkets and subway stations to further extend the reach and service hours of its banking consultation. Altogether, this strategy gives the bank a ubiquitous presence and creates real differentiation in the way it caters to its customers’ needs.

Hana Bank’s Push for Mutual Growth

Another participant in the retail-banking alliance trend is Hana Bank. The necessity to close branches but maintain financial service access, especially in rural areas, was the primary consideration for the bank’s new strategy. Much like its competitors Shinhan and Kookmin Bank, Hana Bank has also deployed cutting-edge STMs from Hyosung to provide extended services and operating hours, elevate customer experiences, and drive down costs. But most crucially, Hana Bank has made a point to offer more financial services while also supporting their retail business partner.

The bank has deploying Hyosung STMs that can handle nearly 50 different kinds of transactions, including account openings, biometric authentication, and debit card issuance, and more. However, by using the banking services in these retail store locations, customers can accumulate points which can then be used for discounts and purchases at GS25 locations. The result? The bank recorded an average 10,000 transactions per month, more than four times the number they experienced when deploying simple cash dispense/withdrawal ATMs. CU on the other hand also experienced 3 times more visitors and logged a 15.5% increase in checkouts YoY using Hana Bank cards (FETV, 2022). This synergistic approach to the store-branch hybrid format provides greater value to customers and helps both businesses grow.

Retail-Bank Alliances are a growing trend and with net branch closures continuing into the foreseeable future, this new format of banking services distribution is only expected to become more commonplace. As a leader in banking self-service solutions, Hyosung has been there every step of the way to support these leading Korean banks as they look to the new frontier of branch services. Contact us to learn more about what make us the ideal partner for banking innovation and branch transformation initiatives.

Sources:

Financial Supervisory Service (2024) – https://www.fss.or.kr/eng/main/main.do?menuNo=400000

Asia Business Daily (2024) – https://www.asiae.co.kr/article/2024062616010227595

Kyunghyang Shinmun (2022) – https://www.khan.co.kr/economy/finance/article/202205231518001#c2b

Financial Review (2023) – http://www.financialreview.co.kr/news/articleView.html?idxno=23361

Hankyung TV (2022) – https://www.wowtv.co.kr/NewsCenter/News/Read?articleId=A202208010073

Financial Economic TV (2022) – https://www.fetv.co.kr/news/article.html?no=116078